Diving DRAM’s durable dominance

Author: EIS Release Date: Aug 1, 2019

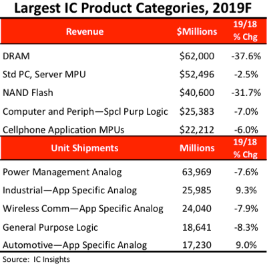

Despite a 38% sales decline expected this year, the DRAM market will remain the largest IC product category in 2019 with sales reaching $62 billion, down from $99.4 billion in 2018, says IC Insights.

IC Insights believes the DRAM market will account for 17% of total IC sales in 2019, compared with 23.6% of the total IC market in 2018.

The NAND flash market is forecast to slip from second to third position in the ranking this year with total sales falling 32% to $40.6 billion.

Taken together, the DRAM and NAND flash memory categories are forecast to account for 29% of the total $357.7 billion IC market in this year compared to 38% of the total IC market in 2018.

Over the past decade, DRAM typically accounted for 14-16% of IC sales and NAND flash memory about 11-12%, but tight supplies of those memories caused average selling prices to climb, which led to surging sales in both segments in 2017 and 2018.

For the first time since the 1990s, DRAM revenues surpassed MPU sales in 2018.

Expected to replace NAND flash at the number two spot in 2019 is the large, mainstream category of microprocessors for traditional PCs, servers, large computers, and a wide range of embedded-processing applications.

Sales in this MPU category climbed 11.0% in 2018 to a record-high $53.8 billion as PC shipments grew for the first time in five years, and strong demand raised server shipments to cloud-computing data centers and Internet-based businesses.

The nearly 2.5% slowdown expected in this MPU category for 2019 is mainly the result of a drop-off in global economic growth; uncertainty and market disruptions caused by the U.S.-China trade war, and an oversupply of inventory in data center servers after high growth in 2018.

Computer and Peripheral—Special Purpose Logic and Cellphone Application Processor segments are forecast to round out the top five largest categories, maintaining the same positions each held in 2018. None of the top five largest IC categories is forecast to see sales growth in 2019.

In terms of unit shipments, four of the five largest categories are forecast to be some type of analog device this year.

Total analogue units are expected to account for 55% of the total 301.7 billion ICs forecast to ship in 2019.

Power management analogue devices are projected to account for 21% of total IC units and are forecast to exceed the combined unit shipment total of the next two categories on the list.

Shipments of Automotive and Industrial—Application-Specific Analogue devices are each expected to rise at least 9% this year, even as total analogue units are forecast to slide 5%.